Frequently Asked Questions

Your Health Savings Account (HSA) coupled with a High Deductible Health Plan (HDHP) can help you save money on your medical expenses. By choosing the HDHP you can save significantly on your health care premiums.

General Information

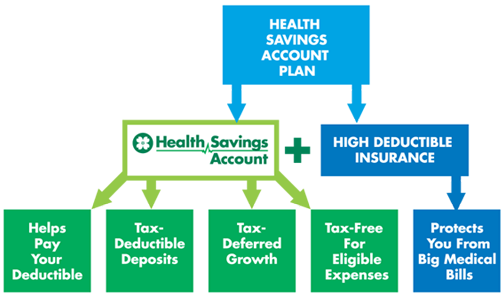

A Health Savings Account (HSA) is what you get when you combine a high-deductible health insurance plan and a tax-exempt savings account. They are designed to allow individuals to use pre-tax dollars to help pay for current and future medical expenses.

HSAs offer a triple tax advantage:

- Contributions are 100% tax deductible

- You choose when to make your contributions and how to invest them

- Contributions to your HSA by your employer are excluded from your gross income

- Unused funds rollover from year to year

- The interest or other earnings on the assets in the account are tax-deferred

- Funds can be used at any time for qualified medical expenses tax-free

Taking money out of your HSA is as easy as taking money out of your checking account. There are no claims to file - you simply swipe your HSA debit card or use Online Bill Pay. If you choose to reimburse yourself for eligible expenses, you can simply make a funds transfer using Online Banking, using Online Bill Pay or withdrawal funds at an ATM.

Yes. Your HSA funds can be used for your spouse and dependent children's out-of-pocket eligible expenses, even if they are not on your health plan.

Yes. The IRS requires your HSA to be an individual account, but you may name other people as authorized signers and they will receive debit cards.

- Contributions are 100% tax-deductible for the account holder (excluding employer contributions)

- Funds grow on a tax-deferred basis and if the funds are used for an eligible expense, the funds are tax-free

- Funds rollover from year to year. Funds used after age 65 are used tax-free for eligible expenses including Medicare premiums or at your normal tax rate for any other reason.

- No use it or lose it rules

- Unspent balances in accounts remain in the account until spent

- Accounts can grow through investment earnings, just like an IRA

Enrollment and Contributions

- Employers and employees can contribute to HSAs as long as the account holder meets the requirements for HSA eligibility

- Family members or any other person can make contributions on behalf of an eligible individual